Kansas City Rail

1997 words 8 minute read – Let’s do this!

TPM 2026 is officially in the books! A big thank you to everyone who stopped by the Port X Logistics booth this year—it was great connecting with so many partners, customers, and new faces across the industry. Safe travels to everyone heading home from Long Beach, and we’re already looking forward to seeing you again next year. If we didn’t get a chance to connect and you’d like to learn more about our services or schedule a demo with our team, reach out anytime at Marketing@portxlogistics.com and we’ll get something on the calendar. Meanwhile, the global logistics landscape continues to evolve. Developing events in the Middle East are beginning to influence shipping networks, with growing security concerns around the Strait of Hormuz prompting some carriers to reassess Gulf calls and routing strategies. Energy markets are also reacting quickly, pushing fuel prices higher and introducing new cost pressures across transportation networks. The result could mean potential surcharges, shifting service loops, and schedule variability across global container services in the weeks ahead. In this update, we break down what these developments could mean for ocean freight, trucking fuel costs, and supply chain planning. And don’t forget to follow Port X Logistics on LinkedIn for real-time insights—or have our Thursday Market Updates delivered straight to your inbox by reaching out to Marketing@portxlogistics.com.

Escalating tensions involving Iran are beginning to ripple across global shipping networks, prompting several major ocean carriers to reassess operations in and around the Persian Gulf. In recent days, some carriers have suspended bookings into certain Gulf ports or diverted vessels away from the region as security concerns intensify. Much of the uncertainty centers around vessel transit through the Strait of Hormuz, one of the most critical corridors in global trade. Even limited disruption in this passage can have outsized consequences for shipping routes and costs, as it handles a significant share of global energy exports and serves as a key gateway for cargo moving between Asia, the Middle East, and Europe.

Although container shipping is less directly tied to the region than energy markets, instability in the Gulf can still carry meaningful implications for global supply chains. If security risks increase, carriers may avoid Gulf calls altogether or consolidate services into lower-risk ports. In some cases, cargo may be offloaded at alternative transshipment hubs such as India, Oman, or East Africa before continuing onward via feeder vessels. These additional handoffs add complexity to already tight shipping schedules and can extend transit times by several days or even weeks. Rising war-risk insurance premiums, longer routing distances, and potential fuel price volatility could also begin feeding into global freight costs across multiple trade lanes.

For U.S. importers, the effects of these disruptions are likely to appear indirectly rather than through immediate cargo shortages. The most common downstream impacts tend to involve schedule instability and network adjustments across global carrier alliances. When vessels are diverted or delayed in one region, disruptions can cascade across entire service loops.

For example, ships operating Asia–Europe rotations that normally call Middle Eastern ports may require schedule restructuring, which can influence vessel availability across Asia–U.S. services as carriers reposition ships to maintain network balance. These adjustments can result in blank sailings, altered port rotations, and inconsistent transit times. Importers relying on tightly scheduled container flows—particularly retailers and manufacturers operating just-in-time inventory models—may experience greater uncertainty around arrival windows and inland transportation planning.

If geopolitical risks persist, importers could also begin seeing gradual shifts in cost structures. Ocean carriers often respond to operational risk with surcharges tied to insurance premiums, security costs, or routing adjustments. These may appear as war-risk surcharges, fuel adjustments, or regional congestion fees tied to alternate transshipment hubs. While each individual charge may be modest, the combined effect can add noticeable pressure to global freight costs.

At the same time, continued geopolitical volatility could accelerate broader sourcing diversification trends. Many U.S. companies have already been expanding supply chains beyond China into Southeast Asia, South Asia, and parts of the Western Hemisphere. Increased instability along key maritime routes could reinforce this shift, gradually reshaping container trade flows and vessel rotations. Ports serving emerging manufacturing hubs such as Vietnam, India, and Indonesia may see increased export volumes as carriers adjust service networks to match evolving trade patterns.

Looking ahead, the trajectory of the market will largely depend on whether current tensions remain contained or escalate further. In a contained scenario, carriers will likely continue operating cautiously while absorbing higher insurance costs and adjusting routing strategies. Under this outcome, the container market may experience periodic schedule disruptions and incremental cost increases but remain broadly functional.

However, if conflict intensifies and begins affecting major maritime corridors or energy exports more directly, the resulting surge in oil prices and marine fuel costs could push global shipping expenses higher across nearly all trade lanes. Elevated fuel prices would likely ripple across the logistics ecosystem, affecting not only ocean freight but also trucking, rail transportation, and drayage operations tied to containerized cargo.

For U.S. importers and logistics planners, the current environment reinforces the importance of flexibility in transportation planning and inventory management. Diversified carrier contracts, multiple routing options, and buffer inventory strategies may become increasingly important to mitigate the risk of sudden schedule disruptions.

In the near term, the global container market appears capable of absorbing localized disruptions thanks to abundant vessel capacity entering the market. Nevertheless, the intersection of geopolitical risk, tariff uncertainty, and evolving trade patterns suggests supply chain volatility may remain a defining theme throughout 2026.

Alongside rising maritime risk, global energy markets have begun responding quickly to instability in the Middle East. Crude oil prices have moved higher as traders factor in potential supply disruptions in one of the world’s most strategically important energy regions. Even the perception of disruption around shipments moving through the Strait of Hormuz can quickly move global oil markets.

For the transportation sector, higher crude prices translate directly into rising diesel and marine fuel costs—two of the largest operating expenses across the logistics industry. Marine fuel accounts for a significant share of ocean carrier operating costs, while diesel typically represents 20–30% of total operating expenses for trucking fleets.

As fuel prices rise, transportation providers across ocean, trucking, rail, and airfreight sectors often adjust fuel surcharges designed to offset those increased operating costs. These adjustments can occur faster than underlying freight rate changes, meaning transportation costs may climb even when freight demand remains relatively soft.

For container shipping, higher oil prices can also influence voyage economics and network planning. Carriers may adjust sailing speeds or routing strategies to manage fuel consumption, which can introduce additional schedule variability. In periods of sustained fuel increases, carriers may also raise bunker adjustment factors (BAFs), gradually increasing the cost of moving containers across major trade lanes.

The trucking industry is typically one of the first segments of the supply chain to feel these effects. As diesel prices rise, fuel surcharges applied to truckload, drayage, and intermodal freight often increase within weeks. While these programs help carriers manage operating costs, they also raise overall landed transportation costs for importers.

Rail transportation can see similar effects. Although rail remains more fuel-efficient per mile than trucking, diesel is still a major operating expense for railroads. Rising fuel costs can influence intermodal pricing and, in some cases, shift the competitive balance between trucking and rail for certain inland freight movements.

For U.S. importers, the combined impact of geopolitical risk and rising fuel prices introduces another layer of cost volatility at a time when many companies are already navigating tariff uncertainty and evolving sourcing strategies. Transportation costs tied to containerized imports can increase through multiple channels simultaneously—including ocean freight surcharges, higher drayage fuel adjustments, and elevated inland trucking or intermodal rates. Looking ahead, the key variable will be how long energy prices remain elevated. If tensions ease and oil prices stabilize, transportation markets may absorb the increase through short-term surcharges without significantly altering capacity dynamics. However, prolonged volatility could lead to higher contract freight rates, tighter trucking capacity in certain regions, and increased pressure on shipping lines to optimize service networks for fuel efficiency. For logistics planners, monitoring energy markets will remain critical. Fuel costs often serve as one of the earliest indicators of broader transportation cost shifts, as price changes cascade through ocean carriers, trucking networks, and inland rail systems before ultimately affecting the total delivered cost of goods.

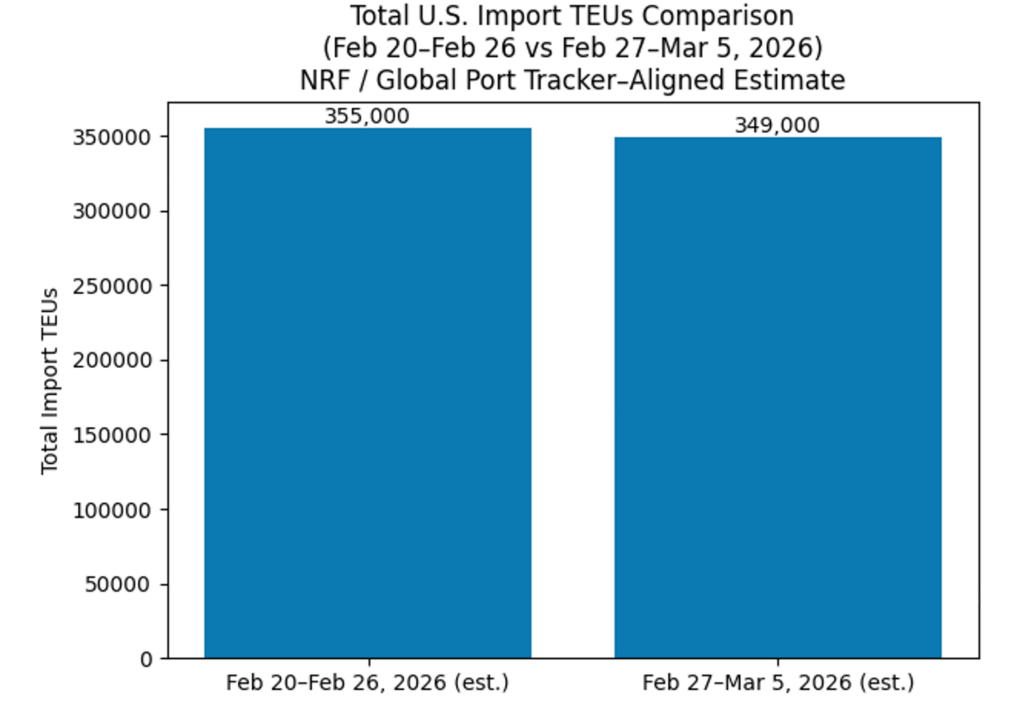

TEU’s are down 1.69% over last week, with majority coming into New York/New Jersey 13.6%, Los Angeles 11.3% and Long Beach 10.9%.