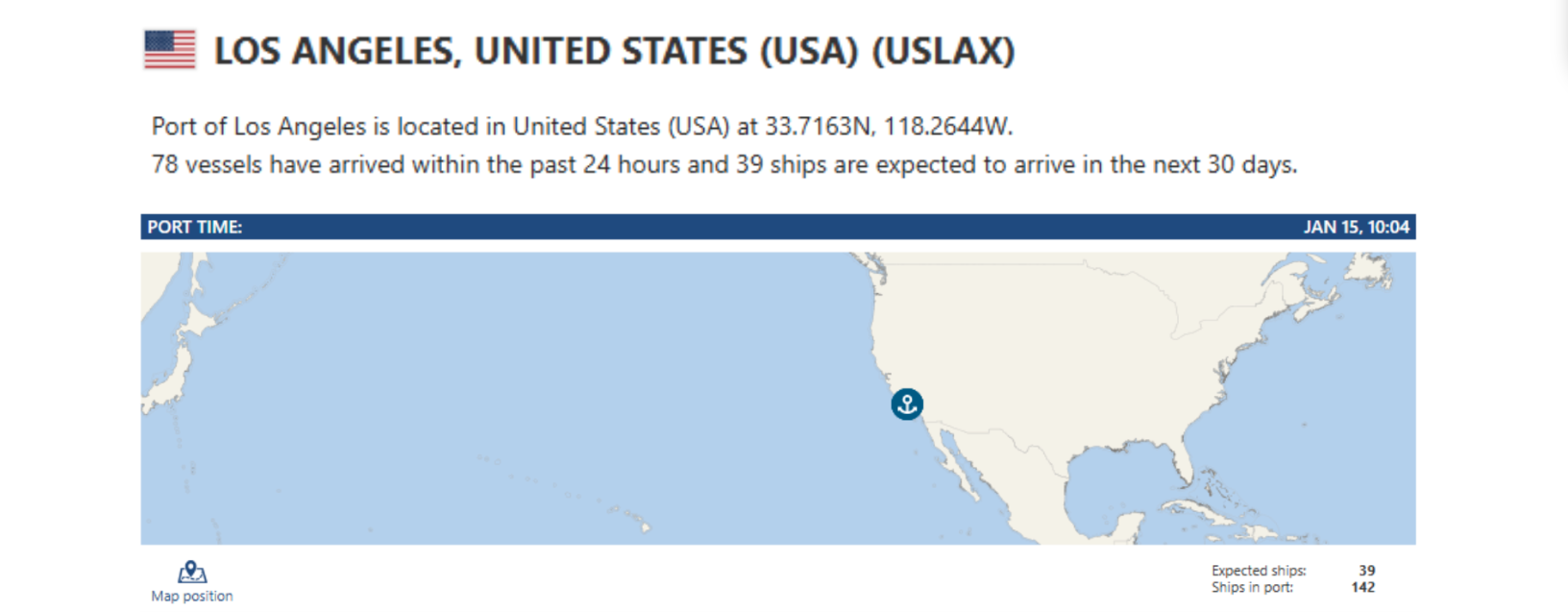

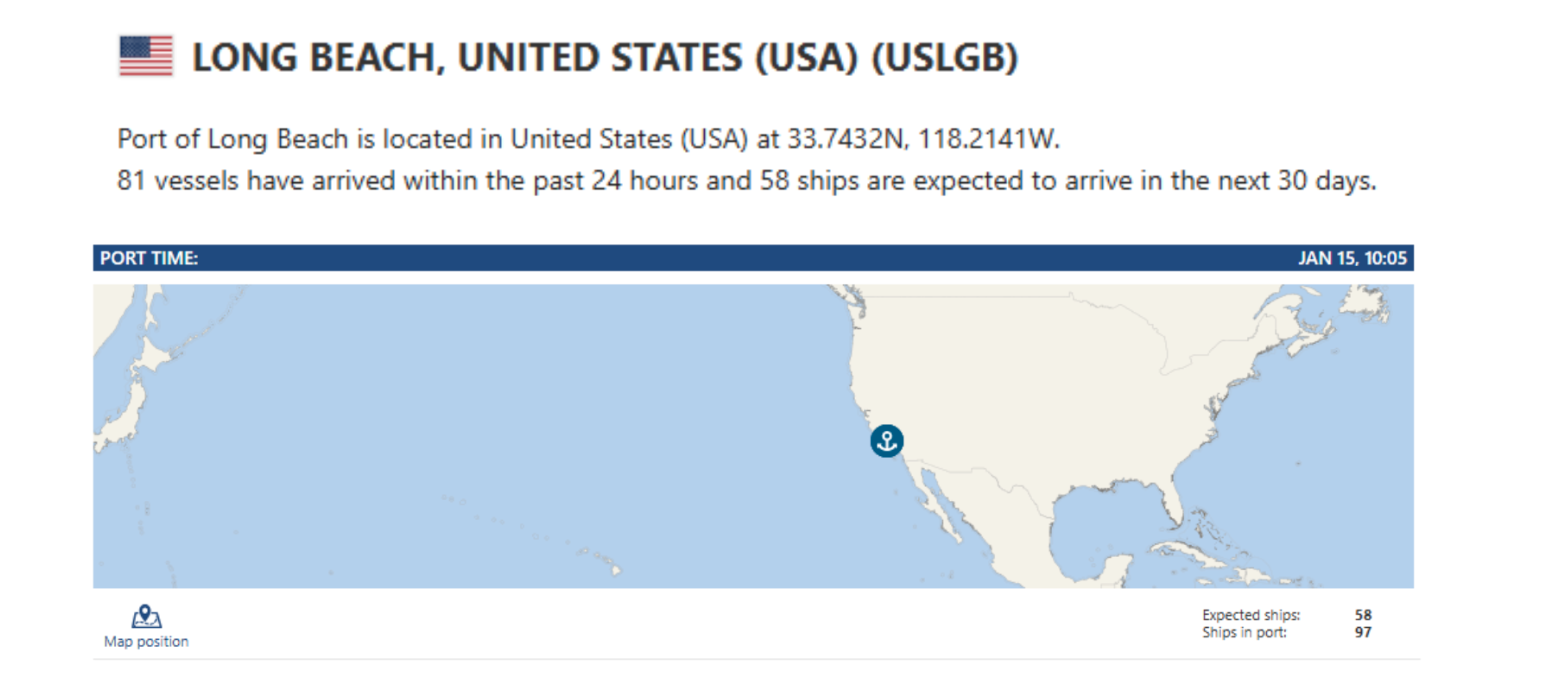

Port of Long Beach

1906 words 7 minute read – Let’s do this!

After months of muted activity, the U.S. container market will start to show signs of movement as January rolls on — though the path forward remains uneven. Late January is expected to deliver the first month-over-month increase in import volumes in some time, driven largely by Lunar New Year cargo pull-forward rather than a fundamental shift in demand. At the same time, year-over-year volumes remain under pressure, cost dynamics are quietly evolving beneath the surface, and global routing decisions continue to reflect a market balancing efficiency against risk. In this week’s update, we break down what’s driving the short-term volume lift, why a broader recovery is likely delayed until later this spring, how import prices and currency trends are influencing landed costs, and what the latest developments in Red Sea routing really mean for transit times and network planning. Don’t forget to follow Port X Logistics on LinkedIn for real-time perspective and market commentary — or get our Thursday Market Updates delivered straight to your inbox by reaching out to Marketing@portxlogistics.com.

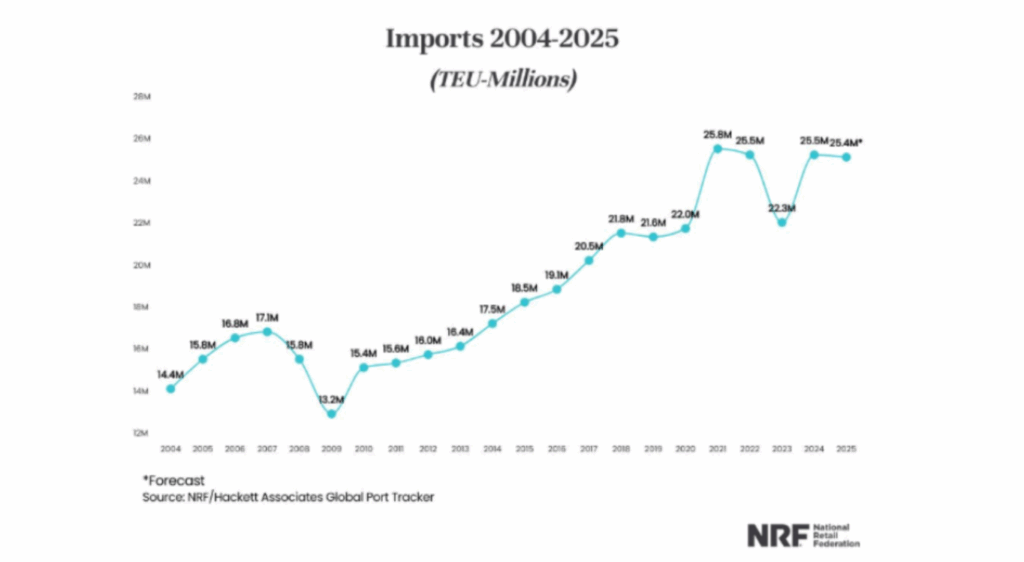

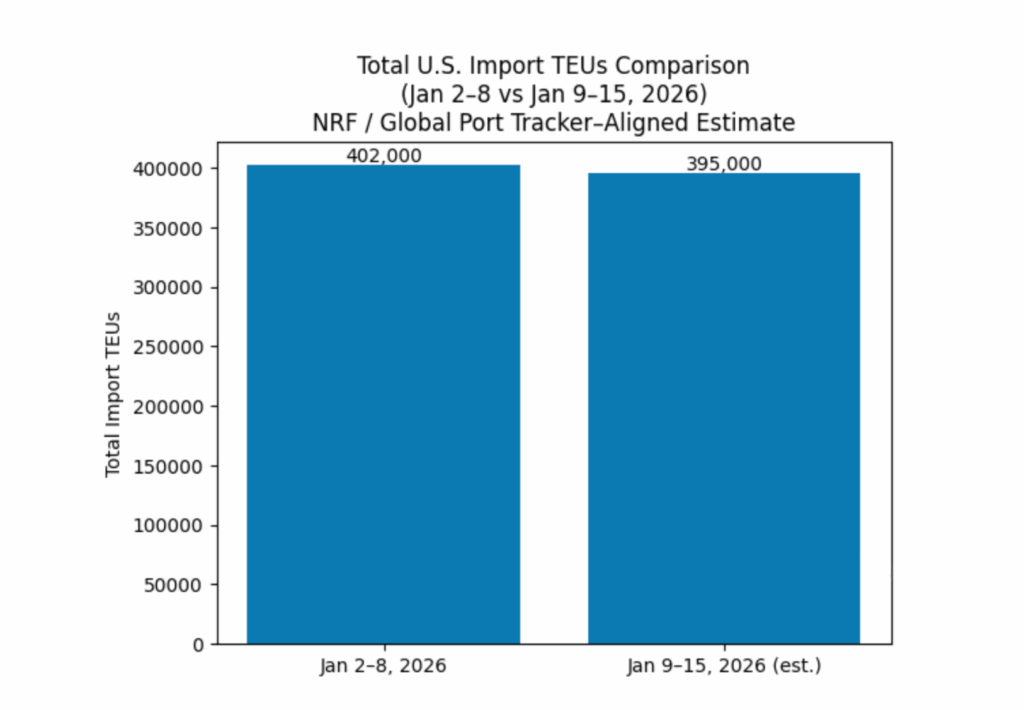

U.S. container ports are expected to record their first month-over-month increase in import volumes this January, according to the latest Global Port Tracker analysis from the National Retail Federation and Hackett Associates. While the uptick marks a shift after several months of decline, overall import levels are still projected to remain below last year’s pace until at least spring. The short-term increase is largely attributed to pre–Lunar New Year shipping activity, which typically pulls some cargo forward ahead of factory shutdowns across Asia, before giving way to the usual post-holiday slowdown.

Looking at the broader picture, U.S. containerized imports totaled 12.53 million TEUs in the first half of 2025, representing a 3.7% increase compared with the same period a year earlier. Despite that early-year strength, full-year volumes are now projected to edge slightly lower, with total 2025 imports forecast at 25.4 million TEUs — down marginally from 25.5 million TEUs in 2024. Monthly projections point to continued year-over-year softness through the late winter, with February and March expected to post notable declines before volumes begin to recover in late spring. Specifically, February imports are forecast at approximately 1.94 million TEUs, followed by 1.88 million TEUs in March and 2.03 million TEUs in April, all reflecting year-over-year declines. A meaningful turnaround is not expected until May, when imports are projected to reach 2.07 million TEUs (Woohoo!) — the first month of positive annual growth since late summer of the prior year. Recent actuals underscore the uneven demand environment, as U.S. ports tracked by Global Port Tracker handled 2.02 million TEUs in November, down both from October levels and from the same month last year.

The magnitude of recent year-over-year declines is amplified by unusually strong import activity in late 2024, when shippers accelerated cargo movements in response to potential port labor disruptions and the threat of new tariffs. According to Hackett Associates, ongoing volatility in U.S. import volumes continues to be driven by trade policy uncertainty, particularly as governments place greater emphasis on protecting domestic industries and addressing perceived trade imbalances. That said, there has been some easing of tensions on the maritime front, with the U.S. and China agreeing late last year to temporarily suspend newly implemented reciprocal port fees as part of broader efforts to stabilize trade relations.

What This Means for Shippers

For shippers, the expected January bump in import volumes is less a signal of sustained recovery and more a timing-driven adjustment tied to Lunar New Year cargo pull-forward. Short-term congestion risks may surface at select gateways, but broader capacity conditions remain relatively balanced as the market moves into the typical post-holiday lull. With year-over-year volumes projected to stay soft through early spring, carriers are likely to continue managing capacity carefully, limiting the likelihood of widespread rate pressure in the near term.

At the same time, trade policy uncertainty remains a key variable. Elevated year-over-year comparisons reflect last year’s surge in early imports driven by labor and tariff concerns — a pattern that could re-emerge quickly if new policy actions are announced. Shippers should remain flexible in routing and timing strategies, closely monitor gateway performance, and be prepared to act quickly if geopolitical or regulatory shifts begin to pull demand forward again. While a more meaningful volume rebound isn’t expected until late spring, disciplined planning and visibility across port, rail, and inland networks will be critical to navigating an uneven first half of the year.